A potential change to the current theatrical window situation was, for a long time, less a question of if, but a question of when. It has always adjusted in the history of movies when a new form of distribution appeared. The rise of streaming services and digital distribution over the last decade intensified the conflict referring to its length between exhibitors and distributors. Multiple attempts to shorten it have failed. Now the disruption caused by the ongoing COVID-19 crisis has sped up the development and a variety of new models are being tested. The central one is the trifecta of deals that Universal struck with AMC and Cinemark in the US and Cineplex in Canada. It allows Universal to release titles, opening to less than a $50 million weekend, to PVOD after just 17 days in cinemas. The window extends to 31 days for titles that open to $50 million and above. These are multi-year contracts and include a share of the PVOD revenue with exhibition.

If this windowing model was industry standard, what could the effect on Box Office be? In an article recently published by Gower Street, we calculated that a median of $2.7 billion Domestic box office was generated after Day 17 in each of the last three years (2017 to 2019). This represents nearly a quarter (24%) of the years’ median total box office ($11.2bn). Our dataset specifically considers English language titles released between 2017 to 2019 with a lifetime box office over $1 million, utilizing data from our partners at Comscore.

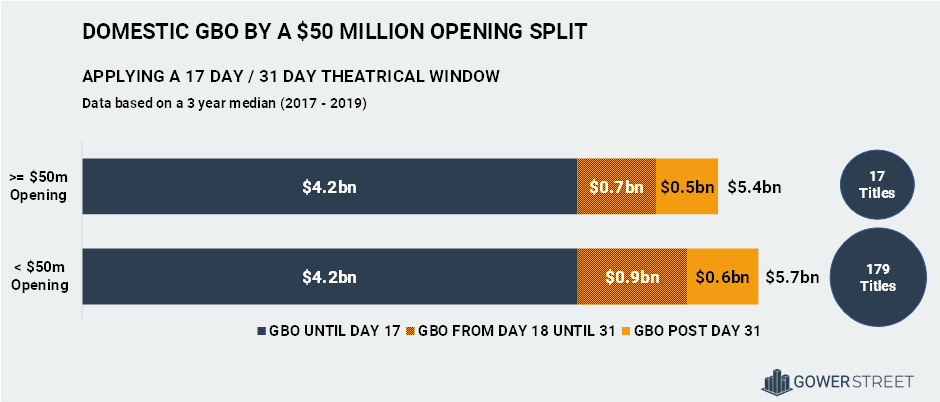

If we apply the lately added $50 million opening criteria, the titles that opened below this amount, generated a total of $1.5 billion after Day 17 (27% of lifetime), while the ones that opened above made $1.2 billion (22% of lifetime). Both clusters of titles had already achieved $4.2 billion of box office each at that point in time. In the period from Day 18 until Day 31 releases that opened to $50 million and above shipped in $670 million. After Day 31 they added another $525 million of box office, representing 10% of this title clusters’ $5.4 billion roll up. That results in $2.1 billion Domestic box office combined being taken by titles that opened below $50 million after Day 17 and by titles that opened to $50 million and above after Day 31. This still represents nearly a fifth (18%) of the years’ median total box office ($11.2bn).

While the cumulative playout between the two clusters doesn’t differ significantly, the main variance is the number of titles in each. While the median number of titles that opened to $50 million and above in each of the last three years (2017 to 2019) was just 17, that number is more than ten times higher with 179 in the cluster that opened below. Mirroring how concentrated box office success is in the theatrical business.

The releases that open to $50 million and above are the successful tentpoles that gross at least $200 million in their lifetime, in more than 60% of the cases. In the last three years, none of these titles ended below the $117 million of THE NUN. Even in this cluster, only a median of five titles a year account for half the box office achieved after Day 31. These are led by family skewed releases like ALADDIN ($64m, 18% of its lifetime GBO), JUMANJI: THE NEXT LEVEL ($61m, 19% of its lifetime GBO) and DESPICABLE ME 3 ($34m, 13% of its lifetime GBO). They are then followed by superhero releases. Among these are BLACK PANTHER ($93m, 13% of its lifetime GBO), WONDER WOMAN ($62m, 15% of its lifetime GBO) and SPIDER-MAN: HOMECOMING ($37m, 11% of its lifetime GBO). And as the one exception to the rule, BOHEMIAN RHAPSODY ($51m, 24% of its lifetime GBO) was part of them. It’s almost certain these won’t be the kind of titles that go straight to PVOD on Day 32.

The bottom section of the $50 million and above openers are more likely to be available on PVOD from Day 32 in the future. Six of the titles in the cluster of 17 account for just 10% of the box office achieved after Day 31 as a median in the last three years. The main driver within this cohort are horror titles. For example, HALLOWEEN ($0.5m, 0.3% of its lifetime GBO), US ($4m, 2% of its lifetime GBO) and IT: CHAPTER TWO ($9m, 4% of its lifetime GBO). Followed by later franchise entries like WAR FOR THE PLANET OF THE APES ($9m, 6% of its lifetime GBO) and PIRATES OF THE CARIBBEAN: DEAD MEN TELL NO TALES ($12m, 7% of its lifetime GBO). Finally, spin-off franchises are in this frontloaded performing group too. FANTASTIC BEASTS: CRIMES OF GRINDELWALD ($7m, 4% of its lifetime GBO) and HOBBS & SHAW ($15m, 8% of its lifetime GBO) to name two.

Within the releases that open below $50m, also just a few account for the major part of the $1.5 billion generated after Day 17. Half of that box office is achieved by just 17 of the titles in that cluster of 179 as a three year median.

Q4 releases are responsible for a significant part of this. Among a few others these are mainly awards contenders that open with a limited release. For example, GREEN BOOK ($70m, 83% of its lifetime GBO), DARKEST HOUR ($55m, 98% of its lifetime GBO) and JOJO RABBIT ($28m, 85% of its lifetime GBO). Besides Q4 releases, break out titles are the next biggest contributor to that group. Memorable examples include GET OUT ($63m, 36% of its lifetime GBO), SPLIT ($39m, 28% of its lifetime GBO) and HUSTLERS ($23m, 22% of its lifetime GBO). Making long-running movies such as these available on PVOD from Day 18 in the future is a complex question and might be considered only in rare cases.

Instead for big budget, fast burn releases that underperform, a Day 18 PVOD offer could be an attractive option. Titles like ALIEN: COVENANT ($6m, 8% of its lifetime GBO), PACIFIC RIM: UPRISING ($4m, 7% of its lifetime GBO) and GHOST IN THE SHELL ($3m, 8% of its lifetime GBO) didn’t benefit at the box office from a longer exclusive theatrical window. Transferring the theatrical buzz into an early PVOD release could have helped to reduce the loss and work as a safety net.

Currently windowing agreements like the one from Universal with AMC, Cinemark and Cineplex are ensuring that titles get theatrically released at all. In the volatile COVID-19 landscape it’s hedging losses for distributors and keeping at least some cinemas open. As it’s a multi-year agreement, it’s there to stay even after the Pandemic and will shape the future of theatrical distribution. The upcoming months are a testing ground to evaluate the potential of multiple windowing approaches to uplift revenue streams. How they need to be shaped, and which is the most appropriate for each title. Other – even more radical – models are being tested as well, with the day-and-date Domestic release of WONDER WOMAN 1984, the sequel to a Domestic $400m+ property.

This article was originally published in Screendollars’ newsletter #145 (November 30, 2020).