The accelerating trend of recovery over the few last months ground to a halt in August. After reaching a pandemic-era peak with $3.37 billion in July, August achieved a global total of $2.37 billion. The month ranked in the middle of the current year so far both in terms of the total box office result (#4 out of 8) and its percentage deficit compared against the pre-pandemic three-year average (2017-2019) with -38% (#5 out of 8).

As expected, August marks the start of a more challenging phase. The impact of a weaker release calendar in August (and heading into September and early October) has started to become evident. Having been closing the deficit against the pre-pandemic three-year average through May, June and July the 2022 box office in both the Domestic and International (exc. China) markets witnessed a slight regression month-on-month. At the end of August, the domestic market was -32% below the three-year average for the running year. That comes after cutting the deficit to -31% in July, down from -47% at the start of May. The International (exc. China) market stands at -30% now, following the reduction from -42% to -29% in the May to July period.

Despite slowing down, the global box office in August was still a third higher than in the same month last year ($1.8bn). However, five of the 30 territories tracked in our global State Of The Market report were down on August 2021. All of them are in Europe: UK/Ireland (-3%), France (-6%), Germany (-7%), the Netherlands (-26%) and Russia (-66%). The last one of course still lacks new blockbuster product due to the aggression-caused US studio boycott in place since March this year. In 2021, the majority of European markets were forced to keep their cinemas closed for most of the first half that year.

With two thirds of 2022 now gone, 23 of our 30 tracked territories have already exceeded their 2021 full year total and 28 their 2020 total. Only Russia (-59%), China (-48%), Hong Kong (-45%), Taiwan (-16%), UAE (-11%), Japan (-8%), and Singapore (-6%) are still trailing behind their 2021 totals, while Russia (-27%) and Italy (-4%) also trail 2020.

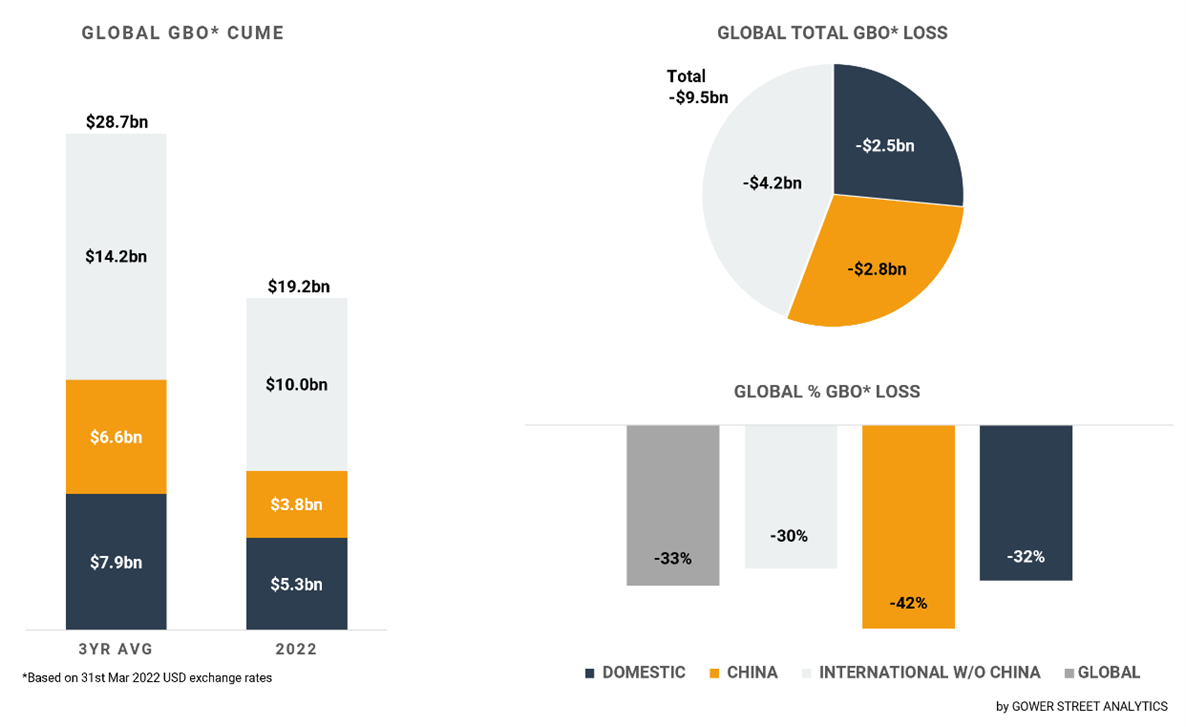

At the end of August global box office stood at an estimated $19.2 billion. This is over $7 billion ahead of the same stage in 2021, but approximately $9.5 billion (-33%) behind the average of the last three pre-pandemic years.

On this month’s GBOT (above), the stacked bar graph on the left shows total box office levels split out by the three key global markets: Domestic, China and International (excluding China). The pie chart indicates the current deficit compared to the average of the past three pre-pandemic years (2017-2019) and where those losses are currently coming from. The bar graph on the bottom right displays the percentage drops globally.

China grossed $582 million in August. For the first time since February, and just the fourth time in the last 12 months, it was the highest grossing market globally. August also marked only the second month in 2022 where China’s box office results exceeded those of the equivalent month in 2021 (+82%).

The month was dominated by local sci-fi comedy MOON MAN, which released on July 29. It contributed nearly half of the August box office with $280m. Its current total of $428.5 million puts it already at #2 of the running year in China. Further local sci-fi comedy WARRIORS OF THE FUTURE generated $92 million and NEW GODS: YANG JIAN – the third film in Ji Zhao’s animated NEW GODS series, did $49 million in August.

While being China’s second highest grossing month of the year so far, it’s just #4 of the year in comparison to the pre-pandemic three-year monthly average (-48%). This is due to August historically being the second most lucrative month in China after February.

The opposite has to be said about the Domestic market. August is historically its third lowest grossing month of the year. With its $479 million, August ranks #6 in the running year. As in China it also ranks #4 in the year in terms comparison against the pre-pandemic three-year average (-39%). Taking that metric, the Domestic market was slightly closer to performing as in pre-pandemic times than China in August. The month’s box office was +13% above that in the same period last year.

In the Domestic market, no title grossed a $100 million or more within the month of August. Only BULLET TRAIN ($80m) and DC LEAGUE OF SUPERPETS ($52m) grossed over $50 million. The majority of box office, besides those two, was generated by holdover titles.

The lack of attractive tentpoles in August also put a break on the performance of the International (exc. China) market, especially in the markets of the world that are most dependent on US product, with a low ratio of local films. The International (exc. China) market delivered an estimated $1.3 billion in July 2022, which is -32% against the three-year average for August. Both metrics rank #4 within 2022 until now. The monthly box office was +26% above that of August 2021.

Regionally, Europe, Middle East, and Africa (EMEA) was hit worse among all sub-regions, bringing in just $551 million. That is the lowest single-month result of the year so far for EMEA. It even came in -6% behind the same month last year! Compared to the pre-pandemic average this August was -36% below.

Latin America struggled as well. Its $124 million, was the second lowest single-month result of the year. Still, that was +57% above the same period in 2021. It was -38% behind the pre-pandemic average for the month.

The sub-region with the best result in August was Asia Pacific (exc. China), which brought in approximately $631 million. This was its third best monthly total of the year and +68% above the same period last year. That was -27% against the three-year average.

Japan was the major driver of APAC’s August performance. It recorded the best single-month box office of the pandemic so far. ONE PIECE FILM: RED was the main reason for that, delivering nearly half of the month’s total. This instalment is the 15th theatrical film in the ONE PIECE franchise, which began in 2000. Opening August 6 it scored the second biggest 2-day opening of all-time, second only to 2020’s record-breaking DEMON SLAYER: MUGEN TRAIN. At the end of August its already the 11th highest grossing local title of all-time in Japan, with a running total of just under $85 million, and the #1 release of 2022.

Of all major global markets Japan is currently the best in tracking against the average of the last three pre-pandemic years for the running year. It’s just -14% behind! However, that number hasn’t changed over the last month. August was, beside of its pandemic-record nature, still -18% behind the three-year average. This was due to the month being historically by far the most lucrative month of the year in Japan.

Despite exceptions like Japan, globally the recovery process definitely slowed down again in August. This will continue for a short period given the reduced frequency of strong US blockbuster product up until October. September is expected to mark rock bottom. Historically being the lowest grossing month of the year anyway, 2022 is unlikely be an exception. As a result, that gap against the pre-pandemic numbers won’t shrink substantially until at least the middle of October. Thankfully this is a temporary issue; not a sign of a decreasing demand, but instead a supply-chain problem caused by pandemic-related delays. Offering numerous blockbusters, the final two and a half months are expected to once again lift the recovery process significantly!

A version of this article first appeared on Screendollars Sept. 3.