Cinemas were in the pink in July as Global box office hit $4.54 billion, delivering the single highest grossing month since before the pandemic began. The result sees July 2023 track a phenomenal +17% ahead of the July-average of the last three pre-pandemic years (2017-2019), according to Gower Street’s latest Global Box Office Tracker (GBOT).

“Barbenheimer” accounted for an estimated $1.23 billion (27%) of the global July total. BARBIE finished the month with an astonishing $810 million after just two weeks as it set its sights on THE SUPER MARIO BROS. MOVIE’s $1.35 billion total in its bid to take the “#1 movie of the year” crown. There was strong support from OPPENHEIMER as it brought in approximately $420 million by month’s end over the same timeframe.

MISSION: IMPOSSIBLE – DEAD RECKONING, PART ONE, which official opened a week earlier following extensive previews in many territories, was actually the second biggest title of the month delivering an estimated $453 million. Two June holdovers from Disney also racking up box office in July were LucasFilm’s INDIANA JONES AND THE DIAL OF DESTINY (approx. $306m) and Pixar’s ELEMENTAL (approx. $238m). Horror INSIDIOUS: THE RED DOOR, which launched at the start of July, brought in $175.5 million by month’s end, making it the biggest title in the five-film franchise to date. There was also a Domestic-only (to date) astonishing run for SOUND OF FREEDOM ($151.4m).

July 2023 also marked the first month since the pandemic began in 2020 that ALL three key component markets that make up the Global picture, Domestic, China, and International (exc. China), tracked ahead of their pre-pandemic averages. The Domestic market delivered an estimated $1.36 billion in July, up +11% on its pre-pandemic July-average ($1.23bn).

The International market (exc. China) was +7% ahead of its pre-pandemic July average ($1.855bn), delivering $1.98 billion in the month. Seven of the top 11 International markets also surpassed their July averages for the 2017-2019 years: UK/Ireland (+18%), France (+14%), Germany (+35%), Spain (+14%), Italy (+98%), Australia (+13%), and Brazil (+5%). Mexico was on par (0%).

China delivered an exceptional $1.2 billion in July, a massive +53% ahead of the country’s pre-pandemic average for the month. Unlike the Domestic and International markets China’s result did not deliver the single highest grossing since before the pandemic, coming fourth. However, this is because it had heavy-weight competition from traditional Chinese holiday windows such as Chinese New Year and Golden Week. The result is remarkable for a period without these major holidays.

While BARBIE and OPPENHEIMER fuelled success across most of the world, China relied largely on its own roster of hits which came thick and fast throughout the month. The market’s top title for July was boxing drama NEVER SAY NEVER ($266m), coming in ahead of June-holdover LOST IN THE STARS ($247.8m within July). Launching two days after NEVER SAY NEVER, and coming third for the month, was historical animation CHANG’AN SAN WAN LI ($213m). The highly anticipated July 20 release of fantasy CREATION OF THE GODS I: KINGDOM OF STORMS, the first part of a trilogy, ranked fourth with $164.6 million. The top 5 was rounded out by comedy drama ONE AND ONLY ($60.6m), which only opened July 28. MISSION: IMPOSSIBLE was the top import title ($46m), ranking 6th overall, while BARBIE also made the top 10 ($26.4m).

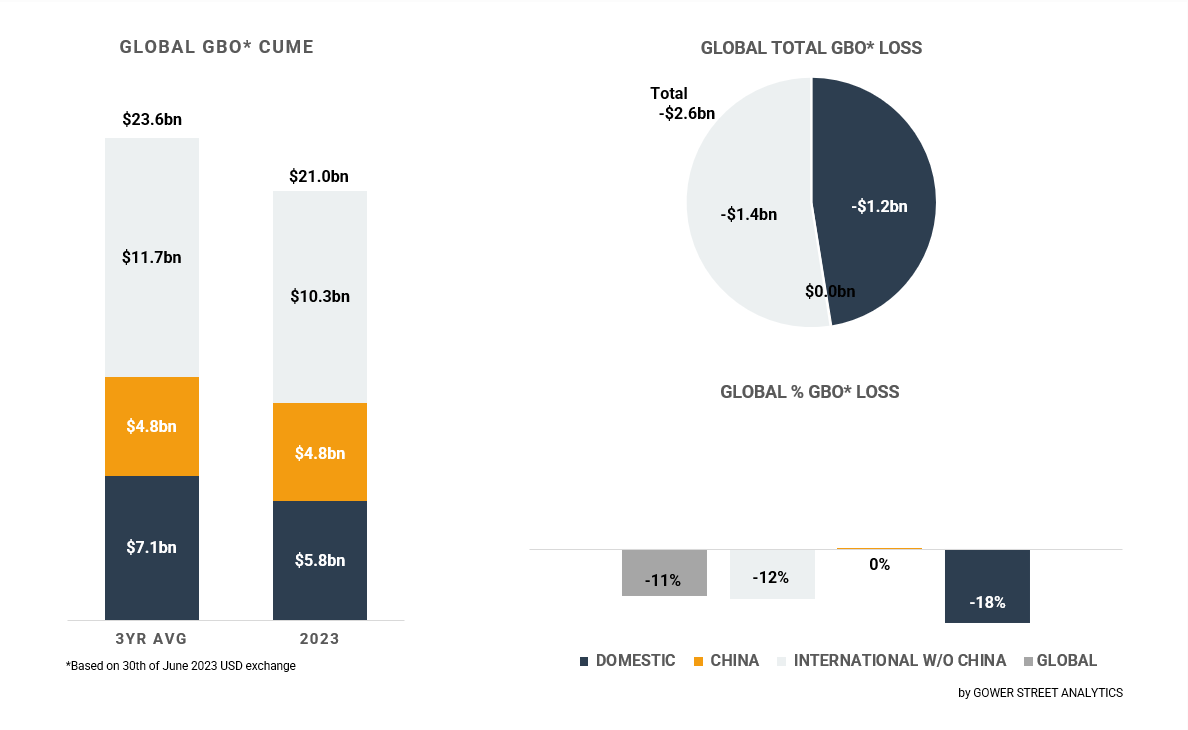

On this month’s GBOT (above), the stacked bar graph on the left shows total box office levels split out by the three key global markets: Domestic, China and International (excluding China). The pie chart indicates the current deficit compared to the average of the past three pre-pandemic years (2017-2019) and where those losses are currently coming from. The bar graph on the bottom right displays the percentage drops globally.

The July success brings the Global box office result through July 31 to an estimated $20.95 billion. This means that after just 7 months 2023 box office is less than 2% behind the full 12-month box office result of 2021. Global box office is currently tracking just -11% behind the 2017-2019 average ($23.56bn), a notable improvement from the -17% deficit shown at the end of June. The first seven months of 2023 were also +31% ahead of the same period in 2022.

China’s 2023 total to date (est. $4.81bn) has already surpassed that market’s full-year 2022 total. The Domestic market has grossed an estimated $5.83 billion through July 31, still -18% behind the average for the last three pre-pandemic years. International (exc. China) has reached $10.3 billion to date, -12% behind the pre-pandemic average. Both the Domestic and International (exc. China) markets have already surpassed their full-year 2021 totals within the first seven months of 2023.

Regionally Europe, Middle East, and Africa (EMEA) has now grossed $5.23 billion after seven months, tracking -12% behind the 2017-2019 average. This follows a remarkable July which grossed $1.02 billion (19.5% of the total year to date) and was +18% ahead of the July-average for the region ($0.865bn).

Latin America is fairing best overall, with 2023 now just -3% behind the average of 2017-2019 following four consecutive months with business tracking ahead of the pre-pandemic average. Boz office to date stands at $1.76 billion. July brought in $0.36 billion, a slimmer +4% gain on the region’s pre-pandemic July-average.

Asia Pacific (exc. China) was the only region tracking behind pre-pandemic business in July with $0.6 billion (-7%). Both Japan and South Korea tracked behind their pre-pandemic averages, -11% and -19% respectively. This was a particular surprise in Japan where the month included the release of Hayao Miyazaki’s latest and final film, THE BOY AND THE HERON, which set a record for the filmmaker and Studio Ghibli on its opening but has not held as strongly as many of his previous films. Despite this Japan still finished July +2% ahead of the pre-pandemic average for the first seven months. Overall Asia Pacific (exc. China) has grossed an estimated $3.32 billion in 2023 to date, -15% behind the pre-pandemic average.

With July showing that markets all over the world can achieve a return to pre-pandemic levels of business with a strong offering of titles to attract audiences the outlook has rarely looked rosier. However, there are thorns on the horizon with the ongoing actors’ strike already resulting in a CHALLENGERS, KRAVEN THE HUNTER and the upcoming GHOSTBUSTERS sequel moving out of 2023. Further release calendar changes are anticipated and should major Q3 and Q4 tent-pole titles such as THE MARVELS, DUNE: PART TWO, WONKA, or THE HUNGER GAMES: THE BALLAD OF SONGBIRDS AND SNAKES also jump ship it could have a negative impact on the year’s final potential.