The first quarters of the past three years were especially impacted by Covid-19 caused restrictions and a lack in supply of attractive global titles. In contrast 2023 opened the year with the highest grossing quarter of the current decade, achieving $8 billion. That is +6% above the prior peak in Q4 2021, fuelled by NO TIME TO DIE and SPIDER-MAN: NO WAY HOME. Q1 2023 was a massive +27% ahead of Q1 2022 and double the first quarter of 2021.

The success illustrates the growing consistency of the recovery, but that doesn’t mean that every month is record-breaking. March added a global total of $2.1 billion and ranks just at #8 of the past 12 months. It’s -36% behind the average of the last three pre-pandemic years (2017-2019). The gap for the year so far is narrower with -23%.

While pre-pandemic levels are still a way off, certain basic levels of recovery are now being largely maintained. For the 15 play-weeks since the 16th of December 2022, at least 23 of the 30 territories tracked in Gower Street’s global State Of The Market report crossed at least Stage 3 of our 5-Stage Blueprint To Recovery on a weekly basis. Stage 3 equals the lowest grossing play-week of 2018-2019 so serves as a base-level for demonstrating consistent recovery. In the same period last year just 4 play-weeks had 23 or more territories crossing that benchmark. This has happened just once since the start of the pandemic in the period from May until early August last year. It was followed by a 10-week period that didn’t reach that benchmark. It is unlikely this will be repeated in the next 10 weeks due to a higher density of the release calendar in comparison.

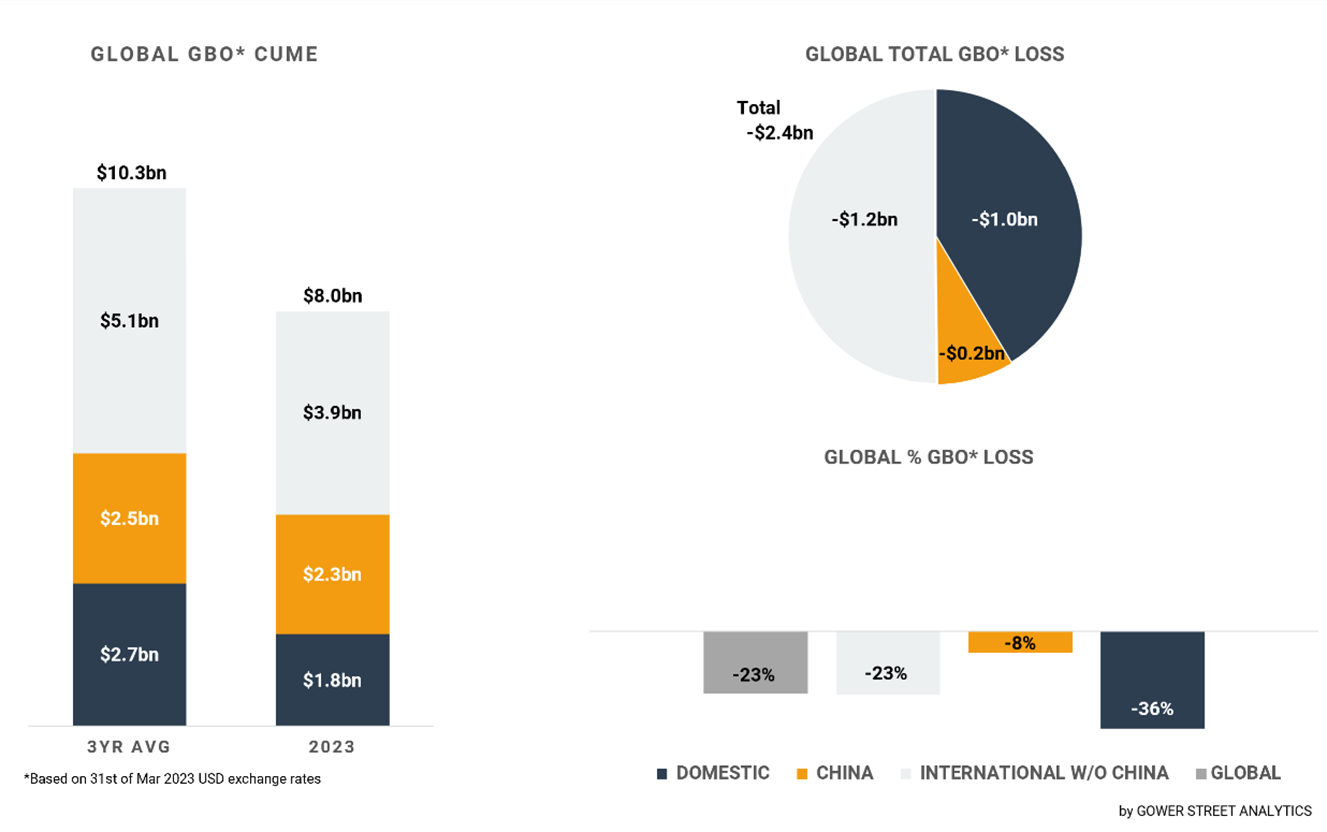

On this month’s Global Box Office Tracker (GBOT, above), the stacked bar graph on the left shows total box office levels split out by the three key global markets: Domestic, China and International (excluding China). The pie chart indicates the current deficit compared to the average of the past three pre-pandemic years (2017-2019) and where those losses are currently coming from. The bar graph on the bottom right displays the percentage drops globally.

The global box office in March was dominated by multiple sequels. CREED III was the biggest movie at the global box office within the month. It has already generated a franchise-best total of $259 million. This is +21% above CREED II ($214m) and +49% above the first CREED ($174m).

JOHN WICK: CHAPTER 4 follows on the heels with a month total of approximately $200 million. It has already out-performed the lifetime totals of both JOHN WICK (+133%, $86m) and JOHN WICK: CHAPTER 2 (+15%, $174m) and should have no problem surpassing CHAPTER 3 – PARABELLUM’s $328 million total.

SCREAM VI delivered approximately $146 million within March. That is already ahead of the successful result of last year’s part 5 (+6%, $138m). Moreover, it’s just a touch behind the original trilogy of movies at that point. Around -10% behind the third part ($162m) and -15% behind the first ($173m) and second SCREAMs ($172m).

Unfortunately SHAZAM! FURY OF THE GODS opened in the other half of the spectrum, coming in significantly behind its prior instalment. At the end of March – after half a month in release – its global cume was at $111 million. That’s a far cry from the $368 million the first part did at the end of its run.

In addition to these new releases ANT-MAN AND THE WASP: QUANTUMANIA’s holdover business added approximately $100 million worldwide in March for a cume of $471 million. While clearly being the highest grossing release of 2023 so far, it is unlikely not only to match 2018’s first sequel ANT-MAN AND THE WASP ($623m) but even the 2015 original’s $519 million!

Geographically the biggest part of the global box office in March was generated across the International market (excluding China) recording a worldwide box office share of 56%, the highest of the year so far. The month came in -30% below the average box office of the last three pre-pandemic years in the same period, slightly increasing the International metric for the year so far to -23%. Its $1.2 billion pushed the 2023 total to $3.9 billion.

The highest grossing sub-region with over half (54%) the month’s International (excluding China) total was Europe, Middle East, and Africa (EMEA). The month came in -28% short of the three-year pre-pandemic average, the same gap as the prior month. Despite this the total EMEA box office was down -5% month-on-month to be the lowest grossing month of the year so far. At the same time the month was up by +15% against the same month last year.

The region was carried by strong performances of multiple major markets. Compared to the three-year average the Netherlands was just down -1%, Austria -9%, Germany -13% and France -18%. It’s the same territories that delivered a lower gap than the regional roll up for the whole first quarter. The Netherlands and Austria are even slightly above the pre-pandemic average by +2%. Germany is -8% behind, while France is down -18%.

As a whole the EMEA region recorded the best quarter since the start of the pandemic. Marginally ahead of Q4 2021 (+0.3%) and +32% above same period last year!

The sub-region of Asia Pacific (excluding China) was able to grow by +43% against the first quarter of last year. But it’s just the 3rd best quarter of the pandemic behind Q2 (-15%) and Q3 (-20%) 2022. March was up +5% on February and -32% down on the monthly three-year average. This increases the metric after Q1 to -24%.

The month of March and the first quarter were led by Japan and Hong Kong in the region. Both are just -8% down against the three-year average after Q1, and -27% (Japan) and -30% (Hong Kong) for the month.

The highest grossing title of March in Japan was the latest in the long-running DORAEMON franchise. NOBITA’S SKY UTOPIA may not have set any franchise records but its cume is already above the last three instalments.

However, it was another Japanese title making big waves outside its home country in March. SUZUME released in Japan last November and grossed over $100 million there up until now. The first five non-Japanese territories it released in March generated approximately the same amount within the month. In South Korea ($26m), Taiwan ($5m) and Hong Kong ($3m) it was the strongest movie of the month. These results are in the ballpark of director Makoto Shinkai’s record-breaking prior hit YOUR NAME from 2017, which delivered around $150 million outside of Japan. SUZUME arrives in the Domestic market as well as across Europe and Latin America from mid-April.

The biggest chunk of SUZUME in March was generated in China. $63 million within the month, which made it the 2nd highest grossing title in March just after local comedy POST TRUTH with $80 million. Both titles were responsible for a bit over half of the month’s soft result of $276 million.

China recorded a relatively weak month after the Chinese New Year (CNY) peak in January and February. March was -54% down against the three-year average and -23% against same month in 2021. Still, it was up against march last year by +109%, when the Covid-19 struggle re-emerged.

The status of the Chinese market after the first quarter looks far more positive due to the very successful CNY period. With a cume of $2.3 billion it’s just -8% behind the three-year average and -12% against same period in 2021. Further it’s up +13% on last year’s Q1.

The Domestic market still operates on a lower level being -36% below the pre-pandemic average after the first three months of 2023 with a total of $1.8 billion. However, Q1 2023 was +29% above Q1 2022.

Thankfully March was showing an upward trend for the Domestic box office. The monthly box office of $647 million was the best so far this year, and ranked #5 among the past 12 months. The positive sign for a broadening range of movies on offer that was visible already in February continued in March. For the first time since February 2020, 13 releases grossed over $10 million in a single month, setting the recovery on a broader ground.

Q1 2023 clearly showed once again that markets that have multiple sources of film supply, being not just dependent on US-studio output, can offer a wide range of content and are generally performing on a higher level. The US-studios offer in the first quarter increased in number and variety. Nonetheless, it lacked family and more female skewing content. It also lacked break-out releases. No Q1 title was able to cross $500 million globally. With the SUPER MARIO MOVIE opening at the beginning of April finally a family movie arrives that should achieve the $500 million mark, expecting a narrower variety at the other end of the month. But ultimately the industry will need a combination of both increased title numbers and variety and major individual box office hits to get back to pre-pandemic heights in the long run.