Theatrical recovery has been occurring at a different pace in markets around the world. Gower Street has been tracking everything that has been happening since March’s almost-global closure; observing growth across different markets and regions. Early growth was slow. Between shutdown and the end of July growth was hard to see, beyond efforts to re-open venues, generating a global box office of just $0.5 billion.

However, from August things started to pick up. Global box office for the month hit $1 billion. September added another $860 million. After six months of growing losses the global box office finally saw percentage loss retract, with box office to the end of September tracking 73% behind an average of the previous three years – a 1-point improvement from the end of August.

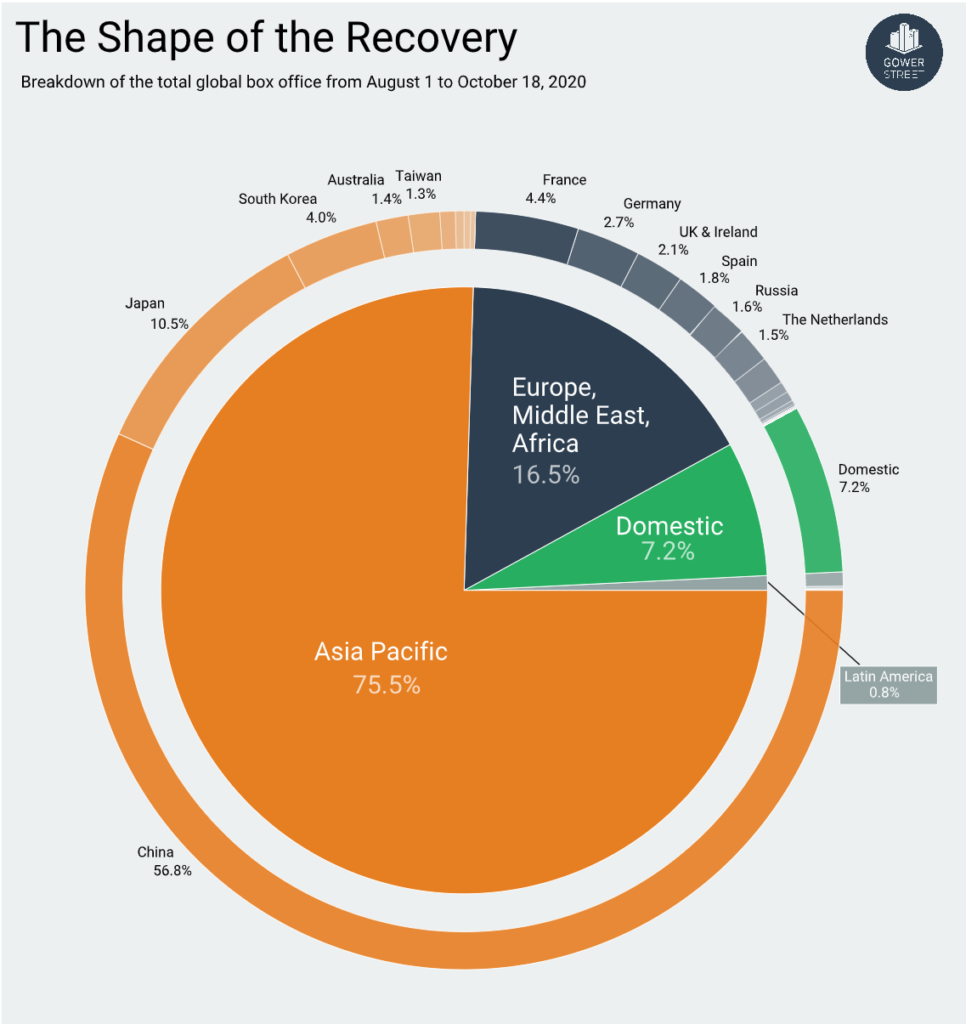

This week Gower Street looks at where the box office made globally since the beginning of August has been coming from, both regionally and by key markets.

Why August?

The near-three months since August have seen the lion’s share of recovery with a total global box office of approximately $2.8 billion. The nested pie graph (above) makes it clear where most of that result has come from with the Asia Pacific region accounting for more than three quarters (75.5%).

China alone has delivered more than half the sum (56.8%), driven by both the massive success of THE EIGHT HUNDRED ($436.6m), release Aug. 21, and the lucrative National Day holiday week at the beginning of October. China, which had re-opened July 20, delivered its first post-lockdown local #1 for the July 31 weekend, resulting is a significant rise in the number of cinemas open by market share heading into August (up from 54% to 73% week-on-week).

But August was also a significant marker elsewhere. The same (July 31) weekend brought significant expansion in UK/Ireland (22% to 45%) and Spain (69% to 82%) in time for the releases of Russell Crowe thriller UNHINGED and Spanish comedy FATHER THERE IS ONLY ONE 2, respectively. Austria’s biggest circuit Cineplexx re-opened Aug. 5).

The first international markets to achieve a Stage 3 (base) level on Gower Street’s Blueprint To Recovery (Japan, South Korea and Taiwan, followed by the Netherlands) had all done in the back-half of July, demonstrating the first real signs of progress. Five further markets would follow in August, mainly thanks to the roll-out of Warner Bros’ TENET – the first, and to date only, Hollywood blockbuster to release post-lockdown. Three more markets, also driven by slightly later TENET openings, would achieve the mark in September.

Cinemas have re-opened at different rates. Some markets, such as South Korea, never completely closed cinemas; others, such as Japan, only did so for a short period; China closed for a full six months; New York, which finally saw its first traditional theaters re-opening this weekend, has been shut down for seven months.

At the start of August only 48% of global theaters were open by market share. By the end of the month it had topped 70%. Gower Street currently estimates 74% of cinemas are open by market share globally, although the number had been as high as 79%.

Major contributors

Markets’ ability to build consumer confidence and find attractive titles to offer audiences, especially in the wake of the post-TENET absence of most Hollywood titles, has also differed.

After China, Japan is the next biggest global contributor, delivering 10.5% – ahead of the Domestic market’s 7.2% share. This week saw Japan become only the second global market, behind China, to achieve all 5 stages of Gower Street’s Blueprint To Recovery – suggesting audience willingness to return has reached a level of full recovery. This was achieved thanks to the smash-hit launch of local anime title DEMON SLAYER THE MOVIE: MUGEN TRAIN, which scored the biggest opening of all-time in Japan, more than doubling the launch numbers of previous record-holder, 2019’s FROZEN II.

France and South Korea both contribute more than 4%; Germany and UK/Ireland over 2%.

The four biggest international contributors (China, Japan, France, South Korea) all share a commonality – each has a robust local production pipeline in normal circumstances. This has enabled these markets to rely on local product to help fill the gap as international markets have felt abandoned by most Hollywood studios.

In it therefore within these markets where the most important growth factor has been seen: the ability to make positive in-roads into market losses and gain ground. Since the start of August, China has decreased its box office deficit against 2019 from 94% to less than 76%. Japan has seen its year-on-year loss shrink from 67.5% to 60% in the same period. France, while significantly smaller, has also seen numbers heading in the right direction, with year-on-year losses reduced from 65.3% to 63.7%.

South Korea’s recovery was hampered by renewed capacity restrictions in mid-August, otherwise it would likely also have seen notable improvement. Despite this the market has still seen a small year-on-year loss reduction since the beginning of August (from 71.9% to 71.1%), thanks largely to the success of the Chuseok (harvest) Festival holiday at the beginning of October.

However, continued delay in Hollywood productions is further endangering even the stronger performing markets. South Korea’s leading exhibitor CJ CGV announced this week that it expects to close 30% of its locations in the next three years as a direct result of the COVID-crisis.

Gower Street’s Road To Recovery reports, tracking all the growth and changes in key markets around the world, are currently available at a special, limited-time, 90% discount offer. Sign-up for subscription by October 31 to access five months of these weekly reports, sent direct to your inbox throughout November 2020-March 2021, at the offer rate. But be quick, the 90% discount offer is only available until October 31. Sign up here: https://gower.st/reports/

This article was originally published in Screendollars’ newsletter #140 (October 26, 2020).